In today’s ever-changing job market, the distinction between 1099 contractors and W-2 employees has become a pivotal point of discussion for both employers and workers. While both play essential roles in the labor market, the nature of their work arrangements, legal responsibilities, and the benefits they receive can significantly differ. In this article, we will dive into the basic disparities between 1099 contractors and W-2 employees, shedding light on the implications of each classification for individuals and businesses alike. We will also explore what you need to know as an independent contractor to help you navigate this unique employment arrangement successfully.

What You Need to Know as an Independent Contractor:

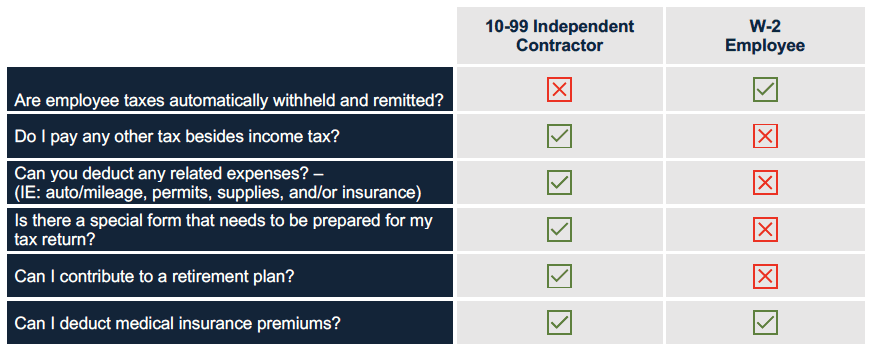

Are employee taxes automatically withheld and remitted?

As a self-employed individual, the responsibility for paying in taxes throughout the year falls to you. The IRS requires quarterly payments be made to avoid a penalty at year end. You will want to ensure that you are remitting both federal and state estimated taxes each quarter. Each estimate can be either a calculation based off your prior year return, or your current year estimated income.

Do I pay any other taxes besides income tax?

Yes, self-employed individuals are responsible for paying income tax as well as self-employment tax. The total self-employment tax is 15.3% of your self-employed income (the Social Security portion of the tax is paid only on the first $160,200 for 2023). You are responsible for paying both the employee (7.65%) and the employer (7.65%) portion of these FICA taxes (for a total of 15.3%). You then get to claim the employer portion of these taxes you are paying (7.65%) as a deduction. You calculate these employment taxes on a Schedule SE attachment to your personal tax return.

Can you deduct any related expenses?

As a 1099 employee you are considered self-employed and therefore eligible to deduct any business-related expenses. Business expenses must be directly related to the earning of income for the business. Some examples would be insurance, permits/licenses, personal property tax, dues, office supplies, tools, fuel, vehicle repairs and maintenance. Capital assets (business vehicles or equipment costing over $2,500) must be depreciated (expensed) over a certain number of years. For example – the purchase of a tractor trailer used exclusively for business would be depreciated over 5 years. If the vehicle cost $100,000, you would expect to deduct $20,000 over a 5-year period. There are some tax laws that allow for accelerated depreciation (such as bonus depreciation) which could help reduce income in the year purchased if applicable.

Is there a special form that needs to be prepared for my tax return?

1099 income is reported on a specialized form called a Schedule C. A Schedule C is a reconciliation of your total 1099 income and expenses for the year. This form will compute what is called your Net Profit or Loss (income-expenses). That total is what is then carried to page 1 of your 1040 and used to calculate your self-employment tax as well income tax. This is not a separate tax return filing, just a separate form attached to your personal income tax return.

Can I contribute to a retirement plan?

The most common form of retirement plan for self-employed individuals is the SEP IRA. SEP IRAs are simple to setup and have lower maintenance fees than that of some other retirement plan options. You can contribute 25% of your net income (total 1099 income-expenses) up to the maximum annual limit (that maximum is $66,000 for 2023). The amount that you contribute for the year is then a deduction against your taxable income on your personal income tax return.

Can I deduct medical insurance premiums?

Yes, self-employed individuals are potentially able to deduct medical, dental and vision insurance premiums you pay throughout the year for yourself, as well as your spouse and/or dependents. Age-based deductions are also allowed for long term care premiums. The eligibility of the deduction is dependent on there being no other health insurance coverage being offered to you (IE: if your spouse’s employer offers health insurance and you are choosing not to participate, the deduction is not allowed) and that your business shows a profit. The deduction would be the greater of total premiums paid for the year or Net Profit shown from the business.

More questions? We’re here to help! Contact a YHB professional today to discuss the tax implications regarding your or your employees’ work status.