One tax planning tip that can be overlooked in year-end planning is possible wash-sale complications for investment holdings if not discussed with your tax or investment professional.

While it can sometimes make sense from an investment or tax perspective to offset your investment losses at year-end with gains you have taken throughout the year, one question remains: Do you repurchase the same security if the market increases before year-end? This is where the issue of wash-sales comes into play. Many individuals can take stock losses each year, but if they buy “substantially identical” securities within a specific timeframe, it could potentially prevent you from taking the usual loss from the stock sale.

The issue of a wash-sale arises when you replace the sold security with a “substantially identical” security either 30 days before or after the date the security was initially sold. This can limit your ability to take the current tax year’s security loss since the loss will be considered a disallowed wash-sale loss and could potentially make your tax liability unexpectedly higher.

An example to illustrate a wash-sale is as follows – Dave buys 500 shares of X Corp. for $10,000 and then sells all 500 shares on June 5th for $6,000, generating a $4,000 loss. Now assume, Dave buys another 500 shares of X Corp. on June 25th for $8,000. Being Dave “bought back” the stock within 30 days after the original sale, he is subject to the wash-sale rules. This means that Dave’s initial stock loss of $4,000 cannot be claimed and added to his new stock basis of $8,000 purchased on June 25th, increasing the new stock basis he bought to $12,000.

One alternative to potentially avoid the wash sale treatment is to repurchase the security outside of the 30-day window before or after your initial security was sold. Another option would be to purchase a separate, but similar security, in the same industry. For example, you could prevent the wash sale treatment from applying if you sold stock in Coca-Cola and replaced it with stock in Pepsi or sold a mutual fund from Fidelity and purchased a different mutual fund from Vanguard.

Some may see wash sales as a disadvantage, but this tax law area has some advantages. If a wash-sale occurs, the basis of the stock sold will be added onto the cost basis of the security bought within the wash sale loss period. Essentially, it gives you a higher starting basis in the new security, meaning if your security increases in value over time, the resulting sale will net a smaller taxable gain in the future.

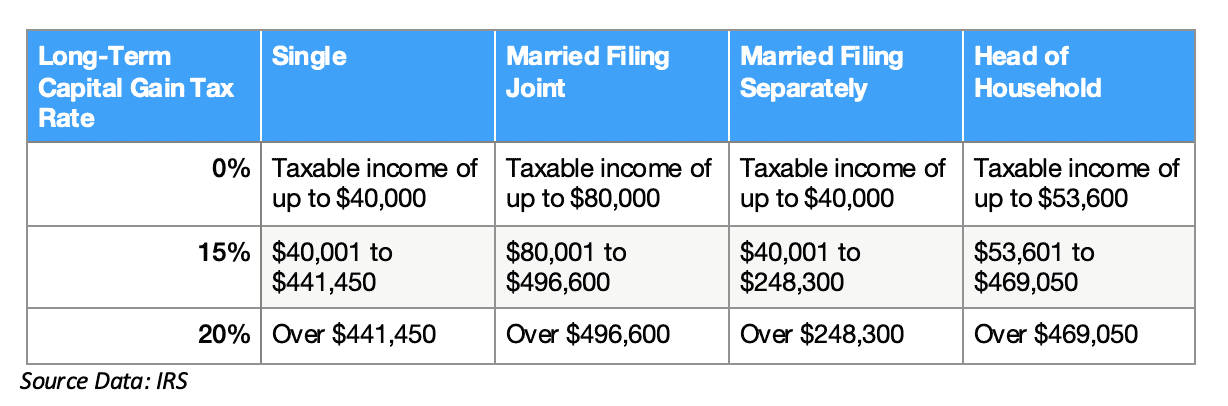

Another potential advantage with a wash-sale is that the initial investment’s holding period is added to the new investment. When you eventually sell the newly bought security, you could qualify for Long Term Capital Gain (LTCG) rates, which would be lower than Short Term Capital Gain (STCG) rates, which are taxed as ordinary income. For a security to be taxed at the preferential LTCG rates, the security needs to be held for longer than one year. Below is a breakdown of the long-term capital rate tables for 2020 and how it could affect your situation.

Need Further Information?

If you have further questions on the complexities of wash-sales or tax law around this area, feel free to contact us to discuss further.