GovCon: Part 3

Establishing Rates for Government Contracts

Understanding your cost pool is vital for all government contractors to succeed in competitive bid situations and remain profitable. This critical understanding keeps you compliant with federal regulations and allows companies to set sustainable rates that drive growth. One of the foundational building blocks for the government contractor’s accounting system is the allocation of costs across contracts. This not only requires the identification of each contract and the deliverables within each contract, but also the proper segregation of direct and indirect costs and the determination of cost pools. The number and composition of cost pools is determined by the contractor, not government regulation.

When preparing a final overhead rate submission, the amounts are clear, the contractor summarizes the actual expenses for the particular year, determines which are allowed and unallowable, and proceeds to summarize them in a format approved by the government. Submitting forecasted rates is a bit unclear, there is no pre-defined format and the expenses need to be budgeted in advance. The expense pools and distribution bases used must produce an equitable distribution of indirect costs to the final cost objectives.

Direct Costs – costs that are identifiable to one specific cost objective, one specific product or deliverable service. These typically include materials, labor and direct subcontractor costs.

Indirect Costs – costs that are related to more than one cost objective, they cannot be identified with a specific cost objective. Examples are rent, utilities, maintenance, supplies, and miscellaneous expenses.

The indirect cost structure established by the contractor should be dependent upon the nature of the contractor’s business environment. The contractor should evaluate functional considerations, off-site versus on-site considerations and management informational needs.

Typical cost structures for rate calculations may include:

1. Fringe benefits

2. Labor overhead

3. Material handling

4. Subcontract administration

5. Service centers

6. General & administrative (G&A)

a. Segment

b. Corporate (home) office

Cost Pool – logical grouping of indirect costs with similar relationships to the cost objective(s), or deliverable(s).

Base – direct activity that will be used to allocate pool costs (causal beneficial relationship). For example, labor is typically a good base for fringe costs.

Indirect Cost Allocation Rate – Cost Pool divided by Base

The same cost cannot be both in your pool and your base.

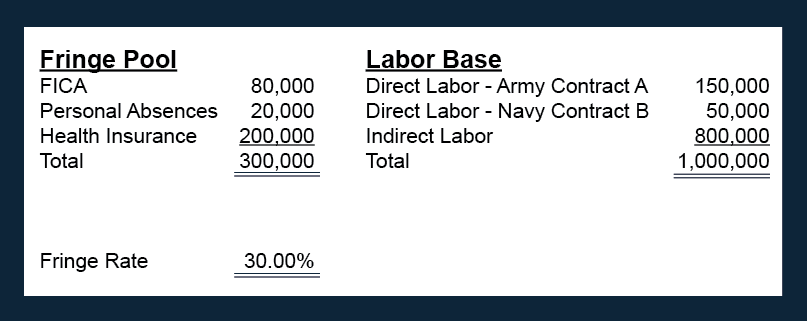

Allocating Indirect Costs – Fringe Example

Given the above assumptions, if labor is your base, then your fringe rate would be 30% ($300,000/$1,000,000). If direct labor costs consisted of $150,000 on Army contract A, you would bill the government $195,000 ($150,000 plus ($150,000 X 30%)).

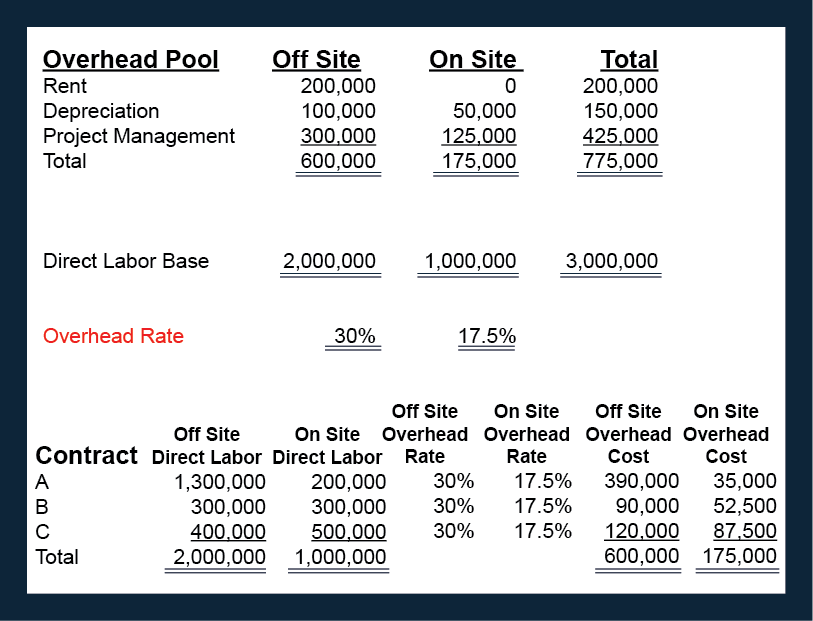

Allocating Indirect Costs – Overhead Example

The above example uses direct labor dollars as the base, however, if more appropriate, the following could also be used as a base for allocation:

- Direct labor hours

- Machine hours

- Production units

- Material costs

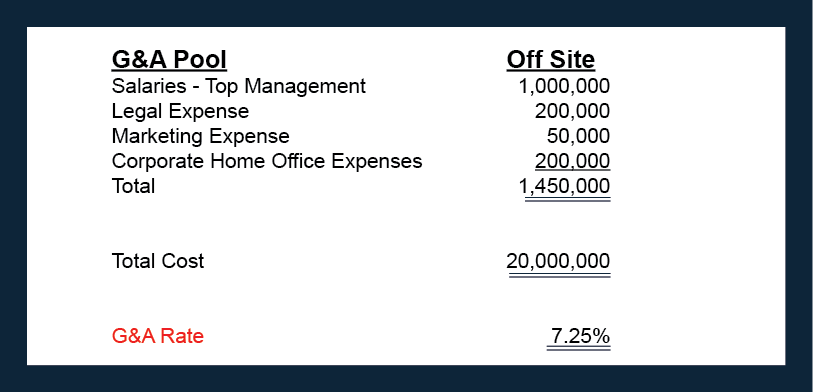

Allocating Indirect Costs – G&A Example

To be included in the Pool Costs for G&A, the expense must be necessary for the overall operation of the company.

Potential Bases to be used to allocate G&A could include:

- Total Cost Input (most common)

- Value Added

- Single Element (rare)

Evaluating and establishing your Company’s cost pools is an absolute necessity to compete in the government contracting arena. Defining your pools and rates cannot only insure you are compliant with government regulation, but also provide you with confidence in bidding jobs properly to maximize profitability.

This article is part 3 of a 4 part series. We will explore the further attributes of different contract types in future articles. If you would like to discuss your current or future contracts and how they may affect the company’s finances, please feel free to contact us.